Roth conversions in 2026 have no income limit and no cap on the amount you can convert. You will pay ordinary income tax on any pre-tax dollars converted, and each conversion starts its own 5-year clock. The One Big Beautiful Bill Act locked in the lower TCJA tax rates, so the urgency has shifted from “convert before rates go up” to “convert while your client’s personal bracket is low.”

If you advise clients on retirement income, Roth conversions can be part of nearly every planning conversation in 2026. The tax landscape shifted dramatically when the One Big Beautiful Bill Act (OBBBA) passed in July 2025, extending the lower TCJA brackets into the foreseeable future. But don’t let the extension of today’s lower tax-bracket rates lull your clients into thinking taxes will stay low forever. There are many demographic, economic and budgetary indicators that higher taxes are coming. Thankfully, OBBBA has given us an extended runway to help our clients prepare.

Keep in mind that here at Stonewood, we’re not CPAs. We build analysis tools to help advisors evaluate the tax consequences and potential tax savings of Roth conversions. Be sure to work with a qualified tax professional on your clients’ individual needs. Below are general considerations per publically-available information from the Internal Revenue Service (IRS).

What Are the Core Roth Conversion Rules in 2026?

A Roth conversion moves pre-tax retirement dollars (from a Traditional IRA, SEP IRA, SIMPLE IRA, or qualified employer plan) into a Roth IRA. The converted amount gets added to your client’s taxable income for that year. Once the money lands in the Roth, it grows tax-free and can be accessed tax-free in retirement.

Here are the foundational rules that govern Roth conversions in 2026:

No income limit. Unlike direct Roth IRA contributions, conversions have zero income restrictions. A client earning $2 million annually can convert just as freely as someone earning $50,000.

No conversion cap. There is no maximum dollar amount for conversions. A client can convert $5,000 or $5 million in a single year. The only practical constraint is the tax bill.

Taxed as ordinary income. The converted amount stacks on top of all other income for the year. A $200,000 conversion for a client already earning $300,000 means the IRS sees $500,000 in total income.

Deadline is December 31. Conversions must be completed by year-end to count for that tax year. Unlike IRA contributions, there is no extension to April 15.

No age restriction. Clients of any age can convert. A 75-year-old taking RMDs can still do a Roth conversion (but must take the RMD first before converting).

Irreversible since 2018. The Tax Cuts and Jobs Act eliminated recharacterization of Roth conversions. Once the conversion processes, there is no undo button.

Key for client conversations: Many clients still think there is an income limit on conversions because they confuse it with the Roth contribution limit. Clarify this early. Conversions and contributions follow completely different rules.

How Much Should Your Client Convert?

One popular conversion strategy in 2026 is bracket filling. You calculate how much room your client has in their current tax bracket and convert exactly that amount. The goal: pay tax at today’s known rate but avoid moving funds into a higher rate.

Using this approach, you might:

Step 1: Estimate the client’s 2026 taxable income before conversion (salary, pensions, Social Security, capital gains, RMDs).

Step 2: Identify which bracket that income falls into.

Step 3: Calculate the gap between current taxable income and the top of the next bracket they’re comfortable filling.

Step 4: That gap is the maximum conversion amount at that rate.

However, for some clients it will make sense to convert funds even if converting those funds pushes them into a higher tax bracket. Why? Through a Roth conversion, we are balancing taxes paid today with potential taxes saved in the future. For many Americans – especially higher-net-worth savers and savers who are concerned taxes will rise in the future – the total taxes paid at today’s rate – even in a higher bracket – might be far less than the total taxes potentially saved through the conversion in retirement. In addition, clients may find that the number of years they use for their conversion can have an impact on total taxes paid and saved.

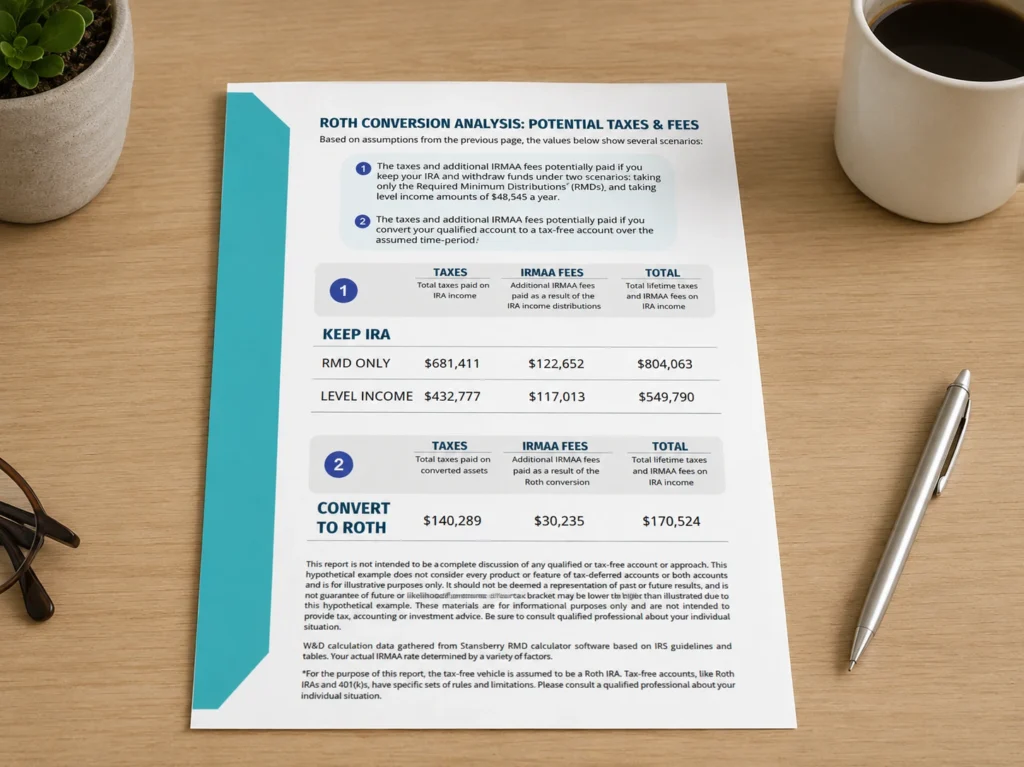

Of course, this analysis is trickier because you have more to analyze. Be sure you have reliable Roth Analysis software like Stonewood’s Roth Done Right analysis to ensure your client isn’t overpaying in taxes today – or leaving potential tax savings on the table in the future.

Make sure you have a compliant report that can show your client their Roth Conversion math in concrete dollars. Saying “you’ll save money” is abstract. Saying “Based on the assumptions we’ve made, his conversion saves you $16,000 in lifetime taxes” lands differently.

The Two 5-Year Rules Every Advisor Should Know

The Roth 5-year rules often trip up savers, because there are actually two separate rules, and they work differently. Getting these wrong can cost clients real money in penalties or unexpected taxes.

Rule 1: The Conversion Penalty Rule

Each Roth conversion starts its own 5-year clock. If a client withdraws the converted amount before that 5-year period ends AND they are under age 59 1/2, they will owe a 10% early withdrawal penalty on the withdrawn funds. The clock starts January 1 of the conversion year, regardless of when in that year the conversion happened. This additional 10% penalty does not apply once the saver is over age 59 ½.

Rule 2: The Qualified Distribution Rule

This rule determines when Roth earnings come out completely tax-free. For any Roth distribution to be “qualified” (meaning no taxes are owed on earnings in the account), two conditions must both be true: the client must be age 59 1/2 or older, AND at least 5 years must have passed since January 1 of the year they contributed to or converted those funds into the Roth IRA.

This is a one-time clock for earnings. Once a client is five years from their initial contribution or conversion , future distributions of earnings are qualified. If your client opened their first Roth IRA in 2020, they already satisfy this rule in 2025. New conversions in 2026 do not restart

How the One Big Beautiful Bill Changes Roth Strategy in 2026

For the past several years, many advisors were encouraging clients who were interested in Roth conversions to convert their funds before taxes went up in 2026. After all, the 2017 Tax Cuts and Jobs Act that lowered tax-bracket rates was set to expire in December 2025.

That changed when OBBBA extended today’s lower tax-bracket rates indefinitely. But the strategic case for Roth conversions didn’t disappear. In fact, we now have an extended timeline to help our clients prepare for potential tax increases ahead. .

Free Advisor Training

Turn Roth Conversations Into Revenue

Watch this complimentary training to learn how leading advisors use retirement tax concerns to create urgency, open Roth conversion conversations, and uncover valuable new planning opportunities.

Get Instant Access to the Training

What Changed

Tax rates are permanent. Today’s lower tax-bracket rates will not automatically adjust. They will remain at today’s current rates until Congress votes to change them.

Standard deduction stays high. For 2026, it’s $32,200 for married filing jointly, adjusted annually for inflation.

Estate tax exemption retained. The higher estate tax exemptions passed in 2017 as part of the TCJA will continue. In 2026, that’s $15M per individual ($30M per married couple)

SALT cap increased. This can slightly reduce the effective cost of conversions for clients in high-tax states who now get a larger state tax deduction.

What Didn’t Change

The fundamental math behind Roth conversions remains the same. Clients still benefit from converting when their current tax rate is lower than their expected future rate. And for many retirees, future rates will be higher – both because of situational changes like RMDs or filing as a single filer if widowed in retirement, and because of legislative changes should Congress need to increase taxes to address our nation’s annual deficit and exponentially-rising debt.

Of course, it’s not just taxes we’re trying to mitigate through a Roth Conversion. For many clients, it’s also IRMAA.

The Medicare Surcharge Trap: IRMAA and Roth Conversions

IRMAA (Income-Related Monthly Adjustment Amount) is a fee that catches many savers off guard in retirement. IRMAA is a surcharge some Americans pay on top of their Medicare premiums to access their Medicare benefits. Medicare uses a special modified adjusted gross income (MAGI) from two years prior to set premium surcharges.

IRMAA can matter in a Roth conversion both during the conversion years and during the retirement years. Retirement funds accessed from a Roth IRA are not generally used in the IRMAA MAGI calculation. So a successful Roth conversion can potentially save both taxes and IRMAA fees for a client.

On the flip side, the additional income assumed during a Roth conversion can potentially trigger or increase IRMAA fees during the conversion period. So it’s important to calculate any additional IRMAA assumed during conversion, and weigh it against potential IRMAA saved in retirement.

If you’re using Roth conversion software, make sure it can also evaluate IRMAA throughout your client’s conversion and retirement. Stonewood’s Roth Done Right software does this for multiple conversion patterns, so your client can see the total amount of taxes and fees paid and potentially saved in multiple scenarios.

Analyze theIRMAA impact of your client’s Roth conversion. The two-year lookback means clients aged 63+ are already in the IRMAA zone for Medicare.

How RMDs Interact with Roth Conversions

Required Minimum Distributions and Roth conversions operate under a strict ordering rule: the client must take their full RMD for the year before converting any additional amount. RMD dollars cannot be converted to Roth. They must come out as a taxable distribution first.

Under current law, RMDs begin at age 73 (moving to 75 for individuals born in 1960 or later, starting in 2033). For some clients approaching RMD age, the years between retirement and 73 can be a prime conversion window. Income is often lower during this gap, creating space to convert at lower rates than RMDs might force later.

The RMD Reduction Benefit

Every dollar converted to Roth also reduces the Traditional IRA balance, which can also reduce future RMDs. A client with $1.5 million in a Traditional IRA at age 73 faces an RMD of roughly $56,600 (using the Uniform Lifetime Table divisor of 26.5). If that client converted $500,000 over the prior five years, the remaining $1 million balance produces an RMD of roughly $37,700. An $18,900 annual reduction in taxable income can compound significantly over retirement.

Building a Multi-Year Conversion Strategy

One large conversion is rarely the right answer. Spreading conversions across multiple years is often preferred to potentially keep the client in lower brackets and avoid additional IRMAA fees..

This is why we consider it a best practice to model your client’s conversion over 3, 5, 8, and 10 years. In fact, we designed Stonewood’s Roth Done Right software to evaluate both the conversion pattern your client suggests and all other conversion patterns between 1 and 10 years. This helps your client make decision information by clear data.

Four Client Conversations That Open the Roth Door

Many clients are worried about taxes, but won’t bring up a Roth conversion on their own. Smart advisors will find ways to open the conversation with clients and prospects alike. the conversation. Here are three scenarios where it naturally fits:

The Early Retiree (Ages 59-72)

“You could be in the lowest tax bracket you’ll see for the rest of your life, sinceSocial Security andRMDs haven’t started yet. We have a window right now to move money from your Traditional IRA into a Roth at potentially lower rates. Want me to run some numbers for you?”

The Client Concerned About Washington

“The tax code is written in pencil, and Congress is constantly changing the rules. I am seeing some real indicators that higher taxes could be coming, from our annual deficit to the size of our national debt. I don’t want your retirement income to be up for vote every two years when we hold elections. Should you look at protecting a portion of your assets from tax changes in Washington?”

The High Earner Who Can’t Contribute Directly

“Your income is too high for direct Roth contributions. But there’s no income limit on conversions. We can move existing Traditional IRA money into a Roth at your current tax rate. If you expect your income to stay at this level or grow, paying the tax now locks in the current rate and creates a pool of truly tax-free money for retirement.”

The Estate-Minded Client

“Your kids will inherit your Traditional IRA and now generally have to liquidate that account within 10 years, thanks to new rules passed in 2019 under the SECURE Act. That means those distributions stack on top of their own income, potentially during their peak earning years. If we convert some of these funds to a Roth now, they can inherit tax-free money instead.”

Three Common Roth Conversion Pitfalls to Avoid

In addition to the pitfalls we’ve outlined above, here are three common pitfalls you can help your clients avoid:

Ignoring state taxes. Federal brackets get all the attention, but state income taxes add 3% to 13% depending on the state. Be sure to model the full combined rate.

Converting in a high-income year without analysis. A client who receives a large bonus, sells a property, or has an unusually high capital gains year might want to delay the conversion. Be sure to evaluate the cost vs. the benefits if your client unexpectedly has a higher-income year than planned.

Forgetting estimated tax payments. Roth conversions don’t have taxes withheld automatically unless the client elects withholding. Your client may need to make

Frequently Asked Questions

Can my client convert a 401(k) directly to a Roth IRA?

Yes, if the client has separated from the employer or the plan allows in-service distributions. The entire taxable amount of the rollover/conversion will be included in income for the year. Many clients roll a 401(k) to a Traditional IRA first, then convert from there. The tax result is identical either way.

Is there a way to undo a Roth conversion?

No. Recharacterization of Roth conversions was eliminated by the Tax Cuts and Jobs Act starting in 2018. Once the conversion processes, the tax obligation is locked in. This makes pre-conversion conversations and analysis more important than ever.

Do Roth conversions affect Social Security taxation?

Potentially. During conversion years, Roth conversion income increases MAGI, which can potentially push more Social Security benefits into the taxable range. Up to 85% of Social Security benefits become taxable above certain income thresholds ($34,000 single, $44,000 married filing jointly in combined income). Many clients, however, already meet the 85% threshold.

Should clients under 59 1/2 avoid Roth conversions?

Not necessarily. The conversion penalty rule only applies if they withdraw the converted amount within 5 years AND before age 59 1/2. If the client plans to leave the money in the Roth for retirement (which is the whole point), the penalty never comes into play. The key question is whether they have enough liquidity outside the Roth to cover the tax bill without touching the converted funds.

How does the Roth conversion interact with the 3.8% Net Investment Income Tax?

Roth conversion income itself is not subject to the 3.8% NIIT because it’s generally considered retirement plan income, not investment income. However, the conversion increases AGI, which can push other investment income above the NIIT threshold ($200,000 single, $250,000 married filing jointly).

Next Steps: Put the Numbers in Front of Your Clients

Roth conversion planning comes down to one thing: showing clients how to minimize taxes and IRMAA during the conversion, so they can maximize tax and IRMAA savings in retirement. . The rules haven’t changed dramatically from 2025, but with the extension of today’s lower tax bracket rates, OBBBA has given us more runway to help our clients prepare.

The advisors who best help their clients successfully execute Roth conversions are the ones who can clearly model the expense and savings of the conversion. Not with a spreadsheet. Not with a verbal explanation. But with a clear, visual analysis that shows the results in real dollars and cents. That’s the kind of analysis that turns a prospect into a client.

Stonewood Financial’s Roth Done Right software was designed to deliver just that kind of report. You input the client’s data, select the conversion scenarios, and the tool builds the presentation for you. We believe it’s the single best tool in the industry to open conversations and close new business.

More than 114,000 reports have been run through the platform, serving clients at all income levels. Try the free Roth Conversion Calculator to see the framework, or request a demo of the full Roth Done Right suite to run analyses during your next client meeting.

Tyler Randall is the National Sales Director at Stonewood Financial. He works with financial advisors across the United States helping them position annuities strategically in retirement plans. Over the past 15 years, he's coached advisors who have written over $400M in annuity premium. His approach focuses on consultative selling, data-driven positioning, and building client confidence through transparency. Tyler is a frequent speaker at industry conferences and webinars.

Real Advisors. Real Results.

See how advisors are using Stonewood software to win larger cases and deliver better

outcomes for their clients.

An advisor was working with a prospect who was a real "do-it-yourselfer" when it came to Roth conversions.

The client was converting assets up their existing tax bracket – and hadn't considered any impact to

IRMAA.

With Roth Done Right, the advisor was able to show an alternate pattern that sped up the conversion to

6 years. The new structure offered $30,000 savings in conversion taxes – a 20% reduction on the

prospect's conversion tax bill. The report also showed hundreds of thousands of dollars in long-term

tax and IRMAA savings from the converted assets – an amount the prospect hadn't been able to quantify

on his own.

Outcome

A new client with $1M in new AUM, and a $1M FIA sale to fund the conversion process.

An advisor was working with a prospect who already had assets with Ken Fisher. Fisher's team presented a

5% systematic withdrawal projection, so the advisor needed a stronger way to frame the income

conversation.

Using the Annuity Alpha report, the advisor showed how an annuity could deliver over 8% in annual cash

flow with lifetime income, plus a long-term care doubler. The contrast was clear enough that the prospect

moved forward.

Outcome

$1.5M placed and a $100K in new business revenue.

An advisor was working with a 58-year-old couple with an established, well-funded retirement income plan,

leaving an additional $3M IRA to build out a legacy for the kids. The couple's existing advisor had no

real additional plan for this money, other than to keep it in their managed account and grow that money as

much as possible for the kids.

Using the Legacy Done Right report, the advisor showed the need for tax planning on this $3M IRA.

According to the advisor, the simple analysis "opened up the wallet" to the Roth conversion story. The

advisor then used the blended Roth/Life feature in the report to show a blend of Roth Conversion assets

with some Life Insurance to help maximize the client’s legacy.

Outcome

$3M in motion. The advisor picked up a $1.5M FIA sale that will be converted to Roth. And the advisor

also sold a 5-Pay Protection focused IUL policy at $225,000 of premium per year.

An advisor group incorporated the Total Tax Burden report into the strategy presentation for all new

prospects. They ran the tax snapshot for every new client as part of their first meeting conversation,

quantifying the growing tax burden of IRA money – and illustrating the kinds of tax savings possible

when working with their firm.

Starting in January of 2023, this simple analysis was presented to every single prospect who walked in

the door. The goal was to differentiate their practice and drive overall revenue growth through various

Roth conversion strategies.

Outcome

From 2022 to 2025, new annual AUM rose from $5M to $50M. Annual FIA sales rose from $3M to $35M.

And annual life premium rose from $50K to $1M.